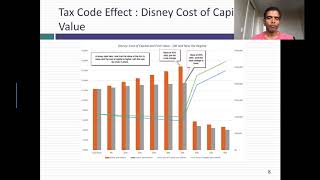

Debt is a source of capital for any business, and in the US, as in much of the rest of the world, the tax code has been tilted in favor of debt for much of the last century. The 2017 tax reform has reduced the tilt significantly by lowering the marginal tax rate and capping the interest tax deduction at 30% of EBITDA (EBIT after 2021). In this session, I use Disney, Facebook and Ford to illustrate the impact on value and cost of capital of the change. I also look at differences in debt loads globally and across sectors.

Slides: http://www.stern.nyu.edu/~adamodar/pdfiles/blog/dataupdate8for2018.pdf

Blog Post: https://aswathdamodaran.blogspot.com/2018/01/january-2018-data-update-8-debt-and.html

Datasets

Debt Ratios by Sector, US (January 2018): http://www.stern.nyu.edu/~adamodar/pc/datasets/dbtfund.xls

Debt Ratios by Sector, Global (January 2018): http://www.stern.nyu.edu/~adamodar/pc/datasets/dbtfundGlobal.xls

Spreadsheets

1. Disney Optimal Capital Structure: http://www.stern.nyu.edu/~adamodar/pc/blog/DisneyTaxReform.xlsx

2. Facebook Optimal Capital Structure: http://www.stern.nyu.edu/~adamodar/pc/blog/FacebookTaxReform.xlsx

3. Ford Optimal Capital Structure: http://www.stern.nyu.edu/~adamodar/pc/blog/FordTaxReform.xlsx

Debt is a source of capital for any business, and in the US, as in much of the rest of the world, the tax code has been tilted in favor of debt for much of the last century. The 2017 tax reform has reduced the tilt significantly by lowering the marginal tax rate and capping the interest tax deduction at 30% of EBITDA (EBIT after 2021). In this session, I use Disney, Facebook and Ford to illustrate the impact on value and cost of capital of the change. I also look at differences in debt loads globally and across sectors.

Slides: http://www.stern.nyu.edu/~adamodar/pdfiles/blog/dataupdate8for2018.pdf

Blog Post: https://aswathdamodaran.blogspot.com/2018/01/january-2018-data-update-8-debt-and.html

Datasets

Debt Ratios by Sector, US (January 2018): http://www.stern.nyu.edu/~adamodar/pc/datasets/dbtfund.xls

Debt Ratios by Sector, Global (January 2018): http://www.stern.nyu.edu/~adamodar/pc/datasets/dbtfundGlobal.xls

Spreadsheets

1. Disney Optimal Capital Structure: http://www.stern.nyu.edu/~adamodar/pc/blog/DisneyTaxReform.xlsx

2. Facebook Optimal Capital Structure: http://www.stern.nyu.edu/~adamodar/pc/blog/FacebookTaxReform.xlsx

3. Ford Optimal Capital Structure: http://www.stern.nyu.edu/~adamodar/pc/blog/FordTaxReform.xlsx

Data Update 8 for 2018: Debt and Taxes

Data Update 8 for 2018: Debt and Taxes

Category :

Tax Debt