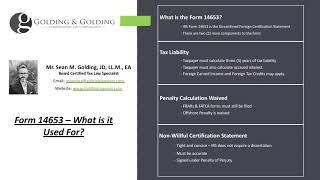

< iframe width =" 480" height =" 320" src =" https://www.youtube.com/embed/YaaIEGnUry4?rel=0" frameborder =" 0" allowfullscreen >< img style =" float: left; margin:0 5px 5px 0;" src =" https://ustaxreview.org/wp-content/uploads/2021/05/c704po.jpg"/ > https://www.goldinglawyers.com. Type 14653: The Type 14653 Accreditation by U.S. Individual Living Beyond the United States for Streamlined Foreign Offshore Procedures, is a really crucial Internal Revenue Service accreditation type used with the streamlined foreign offshore procedures (SFOP). With SFOP, the taxpayer leaves the entire title 26 miscellaneous overseas penalty-- so a lot is riding on the accreditation type.Unlike its foreign counterpart Kind 14654, the 14653 type does not need the applicant to prepare a charge computation, which is utilized in lieu of all the other overseas penalties the Internal Revenue Service can pursue a taxpayer for.The kind is a part of the streamlined filing treatments. These procedures were established to help taxpayers avoid the aggressive federal government enforcement of foreign accounts compliance.Type 14653.While the type 14653 does not require complicated penalty calculations or analysis, it does require a certification that the writing is being made under penalty of perjury. Some dishonest and inexperienced lawyers attempt to misguide applicants about this IRS Form, without offering a full understanding of what perjury suggests.When it comes perjury, it is necessary to note that it is a crime, punishable by jail or jail. That is not to terrify you, however rather to guarantee you understand the seriousness of the submission.Let's have a look at the Kind 14653 to supply some more insight on how a U.S. Individual Residing Outdoors of the United States finishes the form.Leading Area: Personal Details (Type 14653).The leading part of the kind is reasonably simple, and asks only for determining info:.Call.

ITIN/Social Security Number.

Phone number.

Sending by mail Address.

City.

State Zip Code.

Taxes Due (3 Years for Form 14653).The next area is relatively straight forward (at least as to the Taxpayer). It requires details concerning the tax that are due:.Year.

Amount of Taxes Due.

Interest.

Total.Interest is in fact "approximated" interest, because the precise overall quantity of interest is not understood at the time of submission (varies based upon the IRS processing timelines.).What is the Taxpayer Certifying on an IRS Form 14653?The Accreditation part brief but packed with details. A few of the highlights, consist of:.My failure to report all earnings, pay all tax, and submit all required info returns, including FBARs, was because of non-willful conduct. I comprehend that non-willful conduct is conduct that is because of carelessness, inadvertence, or mistake or perform that is the outcome of a good faith misunderstanding of the requirements of the law.".I acknowledge the possibility that modified income tax returns I am sending under the Streamlined Foreign Offshore Treatments might report earnings for tax years beyond the three-year evaluation limitations duration under I.R.C. § 6501( a).Other assessment restrictions durations in I.R.C. § 6501 may permit the Internal Revenue Service to evaluate and collect tax. If I seek a refund for any tax or interest spent for the left out earnings that I am reporting on my modified tax return because I feel that my payments were made.beyond the assessment restrictions duration, I understand that I will forfeit the favorable regards to the Streamlined Procedures. I acknowledge that if the Internal Earnings Service receives or finds proof.IRC 6501 (Limitations on Assessment & Enforcement).The IRS enforcement statute varies from 3-to-6-years, unless civil scams is involved.( a) General guideline Except as otherwise supplied in this section, the quantity of any tax enforced by this title shall be evaluated within 3 years after the return was filed (whether such return was submitted on or after the date prescribed) or, if the tax is payable by stamp, at any time after such tax became due and prior to the expiration of 3 years after the date on which any part of such tax was paid, and no case in court without evaluation for the collection of such tax shall be started after the expiration of such duration.For functions of this chapter, the term "return" suggests the return required to be submitted by the taxpayer (and does not consist of a return of any person from whom the taxpayer has received an item of earnings, gain, loss, deduction, or credit).( e) Significant omission of products: Other than as otherwise offered in subsection (c)--.Earnings taxes: In the case of any tax enforced by subtitle A-- (A) General ruleIf the taxpayer omits from gross earnings a quantity correctly includible therein and-- (i) such amount remains in excess of 25 percent of the amount of gross earnings mentioned in the return, or (ii) such quantity--.( I) is attributable to one or more assets with respect to which info is required to be reported under section 6038D (or would be so required if such section were used without regard to the dollar threshold defined in subsection

< iframe width =" 480" height =" 320" src =" https://www.youtube.com/embed/YaaIEGnUry4?rel=0" frameborder =" 0" allowfullscreen >< img style =" float: left; margin:0 5px 5px 0;" src =" https://ustaxreview.org/wp-content/uploads/2021/05/c704po.jpg"/ > https://www.goldinglawyers.com. Type 14653: The Type 14653 Accreditation by U.S. Individual Living Beyond the United States for Streamlined Foreign Offshore Procedures, is a really crucial Internal Revenue Service accreditation type used with the streamlined foreign offshore procedures (SFOP). With SFOP, the taxpayer leaves the entire title 26 miscellaneous overseas penalty-- so a lot is riding on the accreditation type.Unlike its foreign counterpart Kind 14654, the 14653 type does not need the applicant to prepare a charge computation, which is utilized in lieu of all the other overseas penalties the Internal Revenue Service can pursue a taxpayer for.The kind is a part of the streamlined filing treatments. These procedures were established to help taxpayers avoid the aggressive federal government enforcement of foreign accounts compliance.Type 14653.While the type 14653 does not require complicated penalty calculations or analysis, it does require a certification that the writing is being made under penalty of perjury. Some dishonest and inexperienced lawyers attempt to misguide applicants about this IRS Form, without offering a full understanding of what perjury suggests.When it comes perjury, it is necessary to note that it is a crime, punishable by jail or jail. That is not to terrify you, however rather to guarantee you understand the seriousness of the submission.Let's have a look at the Kind 14653 to supply some more insight on how a U.S. Individual Residing Outdoors of the United States finishes the form.Leading Area: Personal Details (Type 14653).The leading part of the kind is reasonably simple, and asks only for determining info:.Call.

ITIN/Social Security Number.

Phone number.

Sending by mail Address.

City.

State Zip Code.

Taxes Due (3 Years for Form 14653).The next area is relatively straight forward (at least as to the Taxpayer). It requires details concerning the tax that are due:.Year.

Amount of Taxes Due.

Interest.

Total.Interest is in fact "approximated" interest, because the precise overall quantity of interest is not understood at the time of submission (varies based upon the IRS processing timelines.).What is the Taxpayer Certifying on an IRS Form 14653?The Accreditation part brief but packed with details. A few of the highlights, consist of:.My failure to report all earnings, pay all tax, and submit all required info returns, including FBARs, was because of non-willful conduct. I comprehend that non-willful conduct is conduct that is because of carelessness, inadvertence, or mistake or perform that is the outcome of a good faith misunderstanding of the requirements of the law.".I acknowledge the possibility that modified income tax returns I am sending under the Streamlined Foreign Offshore Treatments might report earnings for tax years beyond the three-year evaluation limitations duration under I.R.C. § 6501( a).Other assessment restrictions durations in I.R.C. § 6501 may permit the Internal Revenue Service to evaluate and collect tax. If I seek a refund for any tax or interest spent for the left out earnings that I am reporting on my modified tax return because I feel that my payments were made.beyond the assessment restrictions duration, I understand that I will forfeit the favorable regards to the Streamlined Procedures. I acknowledge that if the Internal Earnings Service receives or finds proof.IRC 6501 (Limitations on Assessment & Enforcement).The IRS enforcement statute varies from 3-to-6-years, unless civil scams is involved.( a) General guideline Except as otherwise supplied in this section, the quantity of any tax enforced by this title shall be evaluated within 3 years after the return was filed (whether such return was submitted on or after the date prescribed) or, if the tax is payable by stamp, at any time after such tax became due and prior to the expiration of 3 years after the date on which any part of such tax was paid, and no case in court without evaluation for the collection of such tax shall be started after the expiration of such duration.For functions of this chapter, the term "return" suggests the return required to be submitted by the taxpayer (and does not consist of a return of any person from whom the taxpayer has received an item of earnings, gain, loss, deduction, or credit).( e) Significant omission of products: Other than as otherwise offered in subsection (c)--.Earnings taxes: In the case of any tax enforced by subtitle A-- (A) General ruleIf the taxpayer omits from gross earnings a quantity correctly includible therein and-- (i) such amount remains in excess of 25 percent of the amount of gross earnings mentioned in the return, or (ii) such quantity--.( I) is attributable to one or more assets with respect to which info is required to be reported under section 6038D (or would be so required if such section were used without regard to the dollar threshold defined in subsection

IRS Form 14653: Streamlined Foreign Certification Form – U.S. Persons Residing Beyond the U S.

IRS Kind 14653: Streamlined Foreign Certification Kind - U.S. Persons Residing Beyond the U S

Category :

Tax Lawyer News